Hi,

Hi,

In this edition, gold cements its status as the world’s most vital financial asset. Daily trading volumes have tripled to $361 billion – eclipsing Treasuries, major currency pairs, and even the top U.S. tech stocks combined. Central banks poured fresh tonnes into reserves throughout March, extending multi-month buying streaks from Beijing to Warsaw. And in a milestone three decades in the making, gold has now overtaken U.S. Treasuries as the largest holding in global central bank reserves. This is no fleeting rally. It is a structural regime shift toward hard assets in an era of geopolitical fragmentation and eroding fiat trust. Read on to see why the golden transition is no longer coming – it is here.

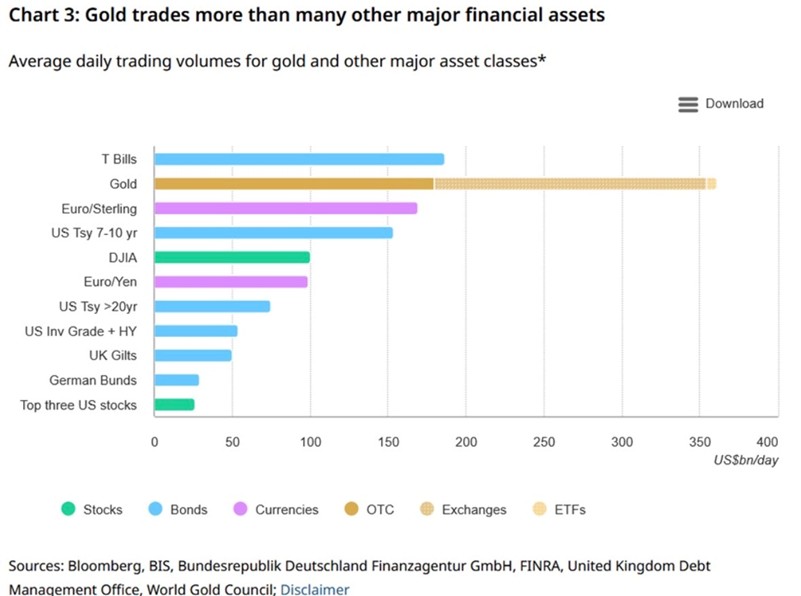

Gold’s Trading Volume Dominance: Outpacing the Financial Elite

Gold is now one of the most actively traded assets on the planet. In 2025, its average daily trading volume reached approximately $361 billion – nearly triple the $134 billion seen in 2021.

That puts gold well ahead of U.S. Treasury bills ($186 billion daily), the EUR/GBP currency pair ($169 billion), and the Dow Jones Industrial Average (~$100 billion). For perspective, the combined daily volume of the three most traded U.S. stocks – Apple, Nvidia, and Tesla – totalled just $26 billion.

Breakdown of gold trades: over-the-counter (OTC) trading accounted for $180 billion, exchanges added $174 billion, and ETFs contributed another $7 billion. This explosive liquidity surge reflects serious participation from sovereign reserve managers, institutions, and global traders – not just retail speculation. When the oldest monetary metal consistently out-trades modern financial giants, it signals deep, structural demand driven by uncertainty, sanctions risks, and fading confidence in paper assets.

Central Banks’ March Buying Spree: Strategic Accumulation Accelerates

While markets watched price swings, central banks kept building their gold positions with discipline. March data highlights continued global diversification:

- China’s People’s Bankadded 5 tonnes – its 17th consecutive month of net buying – bringing reported holdings to roughly 2,313 tonnes.

- Uzbekistanpurchased 9 tonnes, marking its sixth straight month, and lifting Q1 net buying to 25 tonnes.

- Poland’s National Bankincreased reserves by 11 tonnes (per available data), pushing year-to-date net purchases to 31 tonnes and total gold to 582 tonnes.

- Czech National Bankadded 2 tonnes, contributing to a Q1 total of 5 tonnes and overall holdings of 77 tonnes.

- Guatemalabought 2 tonnes – its first addition since September.

Kazakhstan also remained active adding to its reserves following strong February purchases. These moves are part of a broader, multi-year trend: central banks are steadily shifting away from dollar-heavy reserves toward a neutral, time-tested store of value that no single government can control or dilute. The pattern is clear – gold serves as strategic insurance in an increasingly fragmented world.

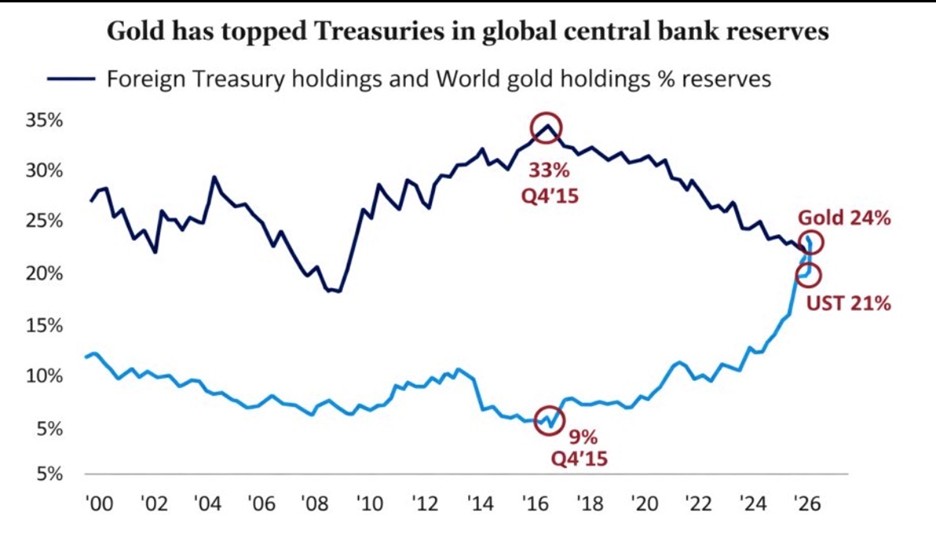

The Historic Milestone: Gold Overtakes U.S. Treasuries in Global Reserves

The numbers confirm what the buying activity suggested. For the first time since the mid-1990s, gold has reclaimed its place as the largest component of global central bank reserves, now accounting for about 24% compared to 21% for U.S. Treasuries.

Long-term charts show the reversal in action: Treasury holdings as a share of reserves peaked near 33% around 2015 before declining, while gold bottomed near 9% that same period and has climbed steadily since 2022. This crossover is highly significant. While the dollar still dominates in trade and short-term finance, gold has become the preferred long-term anchor – liquid, apolitical, and protected from the pressures of rising sovereign debt. The surging volumes and sustained central bank purchases are two sides of the same coin: a quiet but profound reallocation underway.

The Transition Is Real and It’s Only Beginning

From gold’s record trading volumes that dwarf blue-chip equities, to synchronized March purchases across continents, to its historic overtake of U.S. Treasuries in global reserves – the evidence lines up. This is not temporary hype or fear-driven buying. It is deliberate repositioning by the institutions responsible for national wealth preservation.

Geopolitical tensions, persistent inflation risks, and the constraints of ever-growing debt have prompted a return to fundamentals: hard money that cannot be created endlessly. For investors and policymakers alike, gold is transitioning from a tactical hedge into a strategic core asset in a de-dollarizing landscape. Those who recognize this shift early will be better prepared for the decade ahead. The golden era isn’t approaching. It has arrived. Position accordingly.