Hi,

Hi,

In a world of mounting fiscal strain and shifting global powers, the United States stands at a crossroads. A historic debt refinancing challenge, eroding confidence in the dollar, resurgent inflation, and supply pressures in key commodities are converging. These forces are not only testing economic stability but also highlighting the growing appeal of hard assets that can weather uncertainty. This newsletter explores the interconnected risks and the unique opportunity emerging in silver.

The Massive US Debt Maturity Wall

The United States has over seven trillion dollars USD in federal debt maturing in 2026 alone, representing the largest single-year wall of refinancing in modern history. That enormous volume must be rolled over at current interest rates. If the Federal Reserve delays rate cuts, the nation’s interest payments could surge dramatically, and strain budgets further than they already are. Yet cutting rates too aggressively risks overheating an already fragile economy pushing it closer and closer to hyperinflation. Recent Treasury data suggest the actual maturity wall may have approached nine trillion-dollar USD mark when including all marketable securities, amplifying the refinancing pressure and underscoring the tightrope the government must walk to avoid higher borrowing costs or renewed inflation.

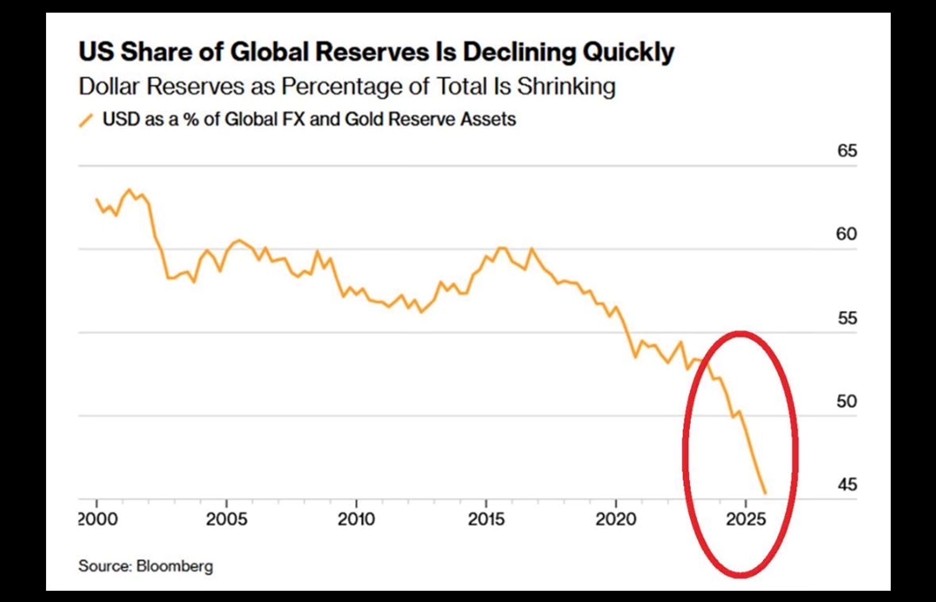

World Distrust of the Dollar and Accelerating De-Dollarization

Global confidence in the US dollar is visibly waning. Its share of global foreign-exchange and gold reserve assets has dropped to around 45 percent, down from more than 60 percent at the start of the decade according to Bloomberg. Even excluding gold, the dollar accounts for roughly 57 percent of FX reserves, the lowest level since 1994, over three decades ago, per IMF figures. Central banks have aggressively diversified away from dollar assets, especially since the 2022 freezing of Russian reserves that highlighted the risks of fiat denominated assets held abroad. Global trade settled in dollars has also fallen to about 40 percent from 54 percent a few years ago, according to SWIFT data.

In this environment, gold has emerged as a preferred alternative precisely because it cannot be overprinted by any government during a crisis. Central-bank gold holdings have now surpassed their Treasury holdings on a valuation-adjusted basis for the first time ever. This shift signals a deeper structural move toward assets that retain value independent of monetary policy decisions.

Inflation Is Back and Only Getting Started

Inflation metrics are flashing warning signs once again. US March PPI inflation (Producer Price Index) climbed to 4.0 percent, its highest reading since February 2023, while core PPI held steady at 3.8 percent. We are now seeing the official US inflation numbers at or above the 4 percent threshold.

Compounding the pressure, fertilizer prices have skyrocketed. Urea, a key input, has risen 87 percent year-to-date and now trades above 720 dollars USD per tonne. With agricultural input costs climbing sharply, food inflation appears poised to accelerate in the months ahead. These pipeline pressures suggest that the recent uptick in producer prices is not a temporary blip, but the beginning of a broader inflationary wave driven by both monetary and supply-side factors.

Silver Market Ripe for Another Price Squeeze

Against this backdrop of debt overhang, dollar weakness, and rising inflation, silver stands out as particularly well positioned. According to the latest World Silver Survey released by Metals Focus and the Silver Institute, the market is heading into its sixth consecutive year of structural supply deficits. The projected shortfall for 2026 alone is around 46 million ounces, with total demand continuing to outpace mine and recycling supply.

Silver prices already reached a record $121 USD per ounce in January, and a prior squeeze in October of 2025 pushed values above $50 USD an ounce for the first time ever amid low London vault inventories and strong buying. While elevated prices last year trimmed some industrial and jewelry demand (solar panel use fell 6 percent), investment buying surged: bar and coin purchases rose 14 percent and net ETF inflows tripled. Forecasts point to further solar and jewelry demand softening this year, yet the underlying deficit remains intact. Unlike gold, silver lacks a central-bank backstop, leaving it more vulnerable to sharp liquidity-driven moves.

The same forces we have examined, a weakening dollar, persistent inflation, and massive structural deficits, make silver an especially compelling asset now. It serves dual roles as a monetary hedge and a critical industrial metal for solar, electronics, and electric vehicles. With governments printing to service debt and central banks rotating out of dollars into gold, silver’s scarcity and industrial tailwinds position it for outsized gains as these pressures intensify.

State of the World Economy

The United States is indeed walking a tightrope with the world economy. The convergence of a historic debt refinancing burden, accelerating de-dollarization, and returning inflation creates a volatile but predictable environment. In such times, assets that cannot be diluted by policy and that benefit from real-world demand, like silver, become strategic stores of value. As deficits widen and trust in fiat erodes, silver’s dual nature offers both protection and upside potential. Prudent investors may wish to consider how this evolving landscape shapes their portfolios in the months ahead.

Stay informed, stay vigilant, and let’s navigate these challenges together in future newsletters.