Hi,

Hi,

For years, investors, businesses, and consumers were told that inflation was under control. Policymakers repeatedly assured the public that rising prices were temporary and that stability would soon return. Yet the latest economic data suggests a very different reality is emerging.

The foundations of the global financial system are being tested once again, and those paying attention are beginning to reposition accordingly.

Inflation’s Unwelcome Comeback

Recent economic data delivered a troubling surprise. April’s Personal Consumption Expenditures inflation rate, the Federal Reserve’s preferred measure of inflation, climbed to 3.8 percent. Core PCE inflation, which excludes food and energy prices, rose to 3.3 percent. Both figures represent the highest readings seen in months and remain dramatically above the Federal Reserve’s long stated 2 percent target. As inflation numbers creep higher and higher the economy gets closer and closer to breaking due to Canada entering a recession. The Bank of Canada can’t hike interest rates when the economy is running slow, but this also allows inflation to run hotter. A reminder, gold and silver perform historically well in stagflation environments.

The significance cannot be overstated. After years of aggressive interest rate increases and promises that inflation was moving back toward normal levels, price pressures appear to be accelerating once again. For households already struggling with rising costs, this raises serious questions about whether inflation was ever truly defeated, which we had always said it was not and that another, stronger wave of inflation was coming. History has shown that inflation rarely disappears quietly. Once it becomes embedded in an economy, it often returns in waves, eroding purchasing power and forcing central banks into difficult decisions.

The concern today is not simply that prices are rising. The concern is that confidence in policymakers’ ability to control those prices may be fading and when this happens you see a rush to hard assets like silver and gold. Something that has already begun behind the scenes.

The Quiet Migration Toward Gold

While headlines remain focused on inflation, a much larger trend is unfolding behind the scenes.

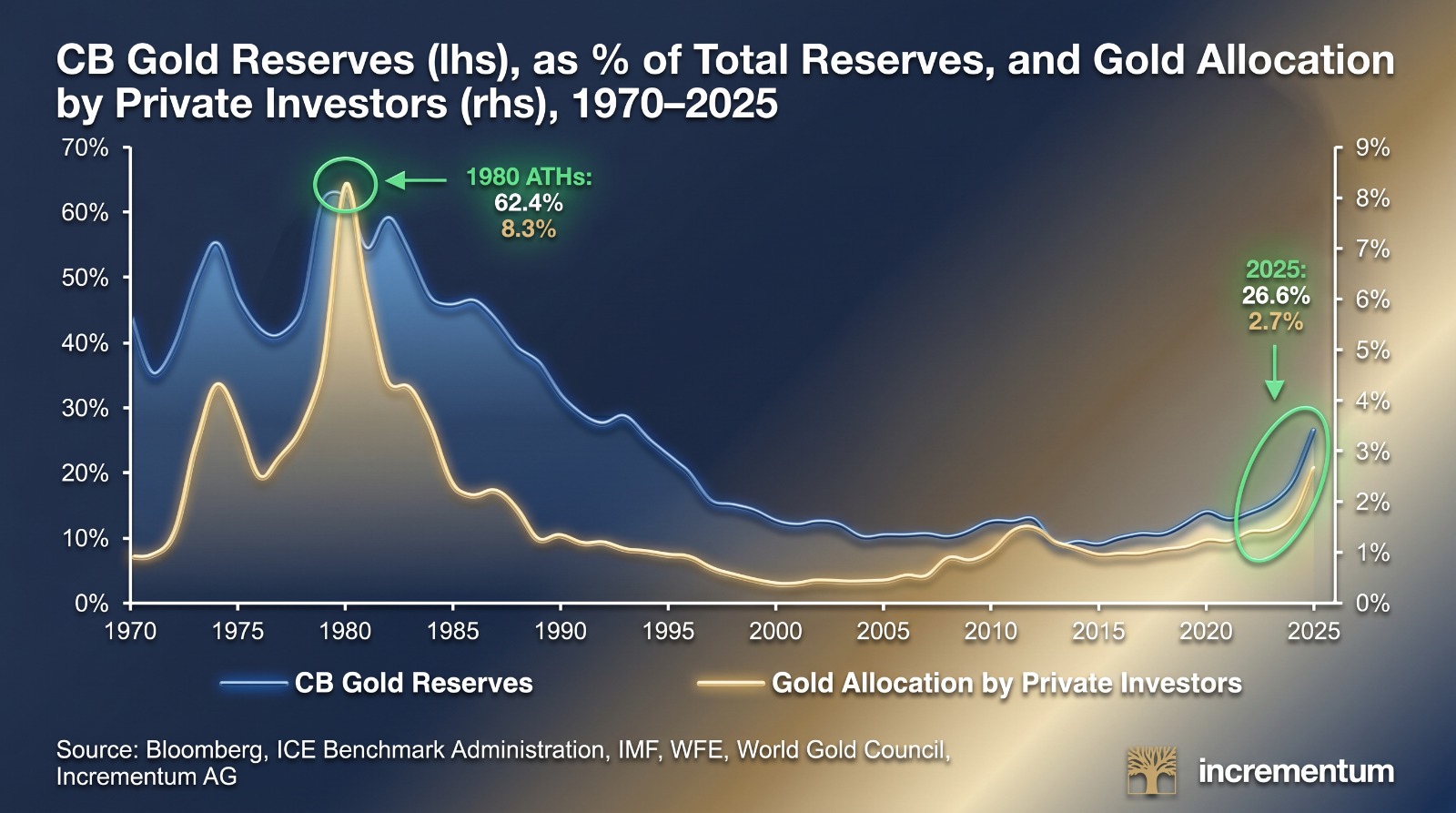

Central banks around the world continue to increase their exposure to gold at a pace not seen in decades. In 2025, gold reserves reached 26.6 percent of total central bank reserves, the highest level since 1993. Since 2013, that figure has surged by an astonishing 17 percentage points.

At the same time, private investors are moving in the same direction. Gold allocations within private investment portfolios rose to 2.7 percent last year, the highest level recorded since 1984. Even more striking, this allocation has more than doubled over the last five years.

This shift toward gold is not occurring because of sentiment or speculation. It reflects a growing recognition that the world is entering a period of heightened uncertainty. Geopolitical tensions, persistent inflation, rising debt burdens, and concerns surrounding government finances have created an environment where traditional assumptions are increasingly being questioned. When both central banks and private investors begin making similar decisions, it is worth asking what they see that others may not.

The Lesson History Keeps Repeating

Financial markets change. Governments change. Monetary systems change. One thing rarely does. Since August of 1971, when the United States formally severed the dollar’s final link to gold, major currencies have experienced a staggering loss of purchasing power when measured against the precious yellow metal.

The U.S. dollar has lost more than 99 percent of its value relative to gold. The British pound has suffered a similar decline. The euro, if measured over the same period, would tell a nearly identical story. Even currencies often viewed as stable, such as the Japanese yen and Swiss franc, have experienced substantial losses against gold over time.

Meanwhile, the price of gold measured in U.S. dollars has risen more than 11,000 percent. This pattern has unfolded repeatedly throughout history. Currencies are created, expanded via the printing press, and eventually weakened through the pressures of debt, politics, and economic necessity. The names of currencies change. The government officials change. The outcomes remain remarkably consistent.

For centuries, societies have rediscovered the same lesson during periods of monetary uncertainty. When confidence in paper money weakens, people begin searching for something that cannot be created with a keystroke. This leads them back to gold and silver every time.

It is true that gold and silver have experienced a choppy year as economic uncertainty continues to build. Yet despite the volatility, gold remains up roughly 3 percent on the year while silver is higher by about 1 percent. At first glance, those gains may not seem particularly impressive. However, a deeper look reveals that both metals have continued to do exactly what they have done for centuries: preserve purchasing power during a period when fiat currencies have steadily lost value, as discussed earlier.

Looking further ahead, many of the world’s largest financial institutions remain bullish on precious metals. Several analysts have projected gold prices reaching as high as $20,000 per ounce by the end of 2026, while Bank of America’s precious metals desk has suggested silver could eventually trade above $300 per ounce. Interestingly, those targets would place the gold-to-silver ratio near the 60-to-70 range where it sits today.

In comparison, Bitcoin, often promoted as “digital gold,” has struggled during the same period. Since January, bitcoin has declined more than 30 percent. Investors who chose bitcoin over physical gold and silver this year have generally not fared as well, highlighting the difference between assets designed by nature to preserve wealth and assets that remain heavily influenced by speculative market sentiment.

What Lies Ahead

The latest inflation data serves as another reminder that the challenges facing the global economy have not disappeared. Inflation remains elevated. Government debt continues to expand aggressively. Central banks are quietly increasing their gold reserves. Private investors are following a similar path. Perhaps the most important question is not whether these trends will continue. It is whether the public will recognize their significance before the consequences become impossible to ignore. History suggests that monetary realities eventually reveal themselves. The only uncertainty is how long it takes for everyone else to notice the change is occurring.